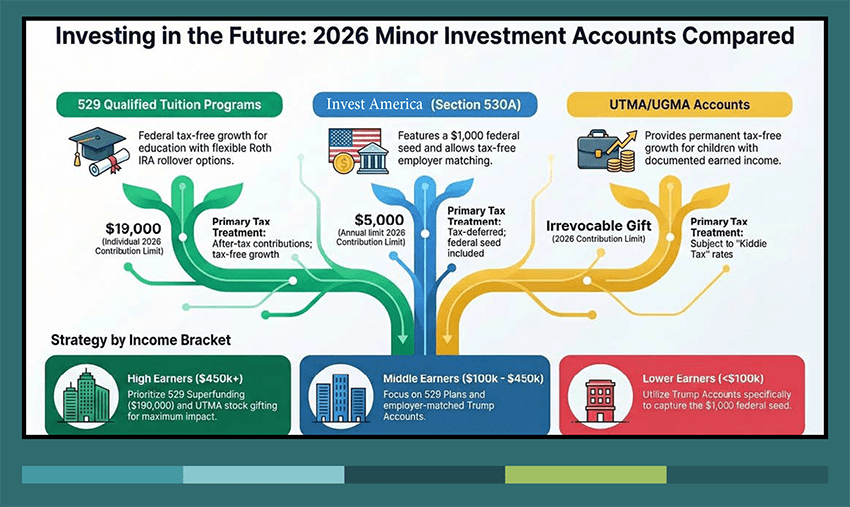

Reviewing the New Savings Programs

Along with H.R.1, a citizen-led ground swell for increasing the percentage of people who own stocks has manifested itself into the recently introduced Investment America Accounts. The backstory of how Brad Gerstner and Michael Dell created and partially funded this concept is here.

Our focus is on how these accounts can benefit you and your family, and to put it in proper context, we conducted a full review of all tax-advantaged accounts. The DLK Minor Savings Report is a comprehensive look at everything from the old UTMA, the evolving 529’s, and the brand new Invest America Accounts. It could be worth forwarding to your family members.

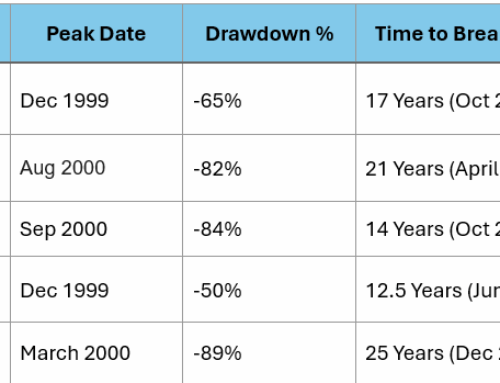

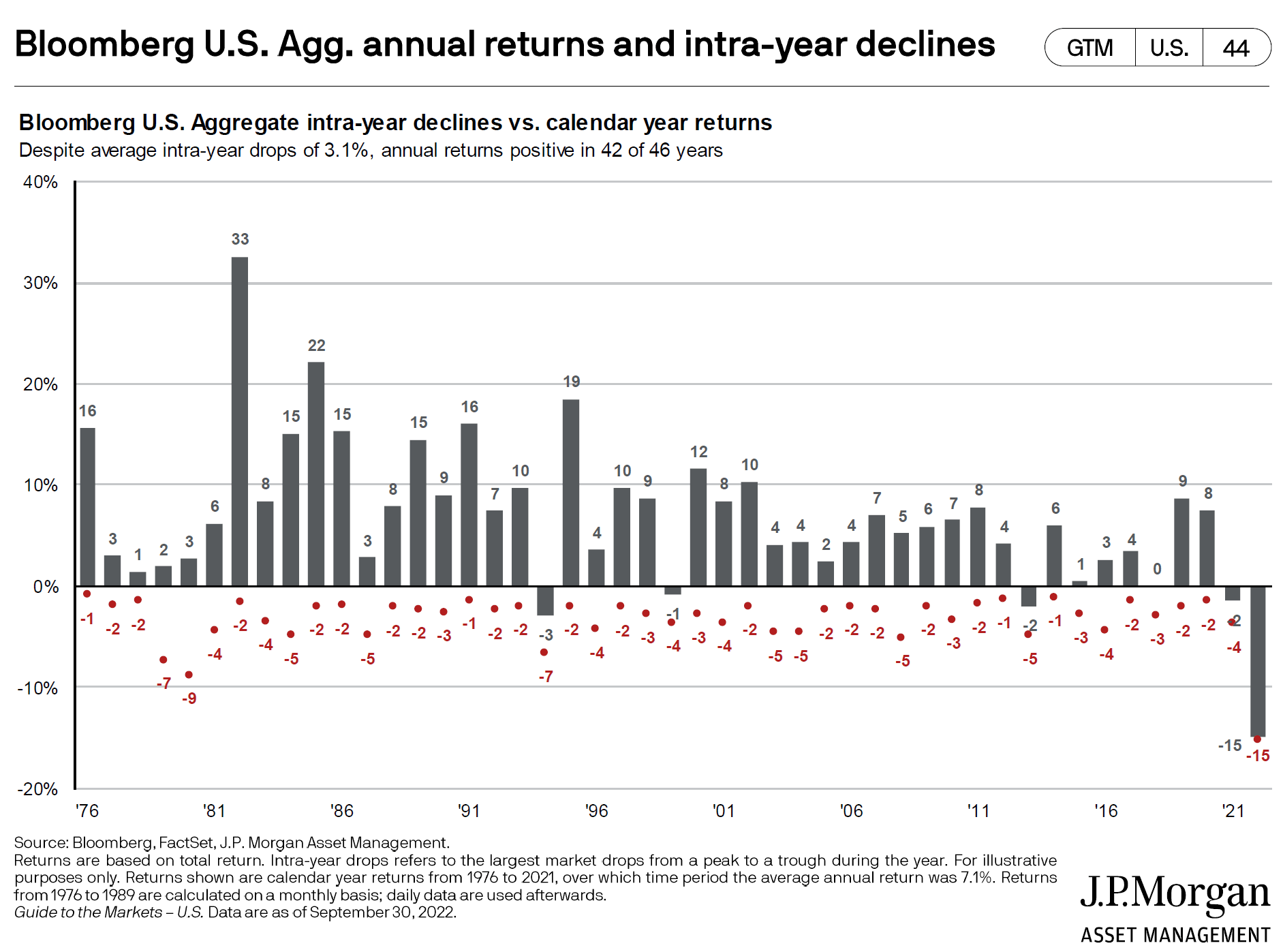

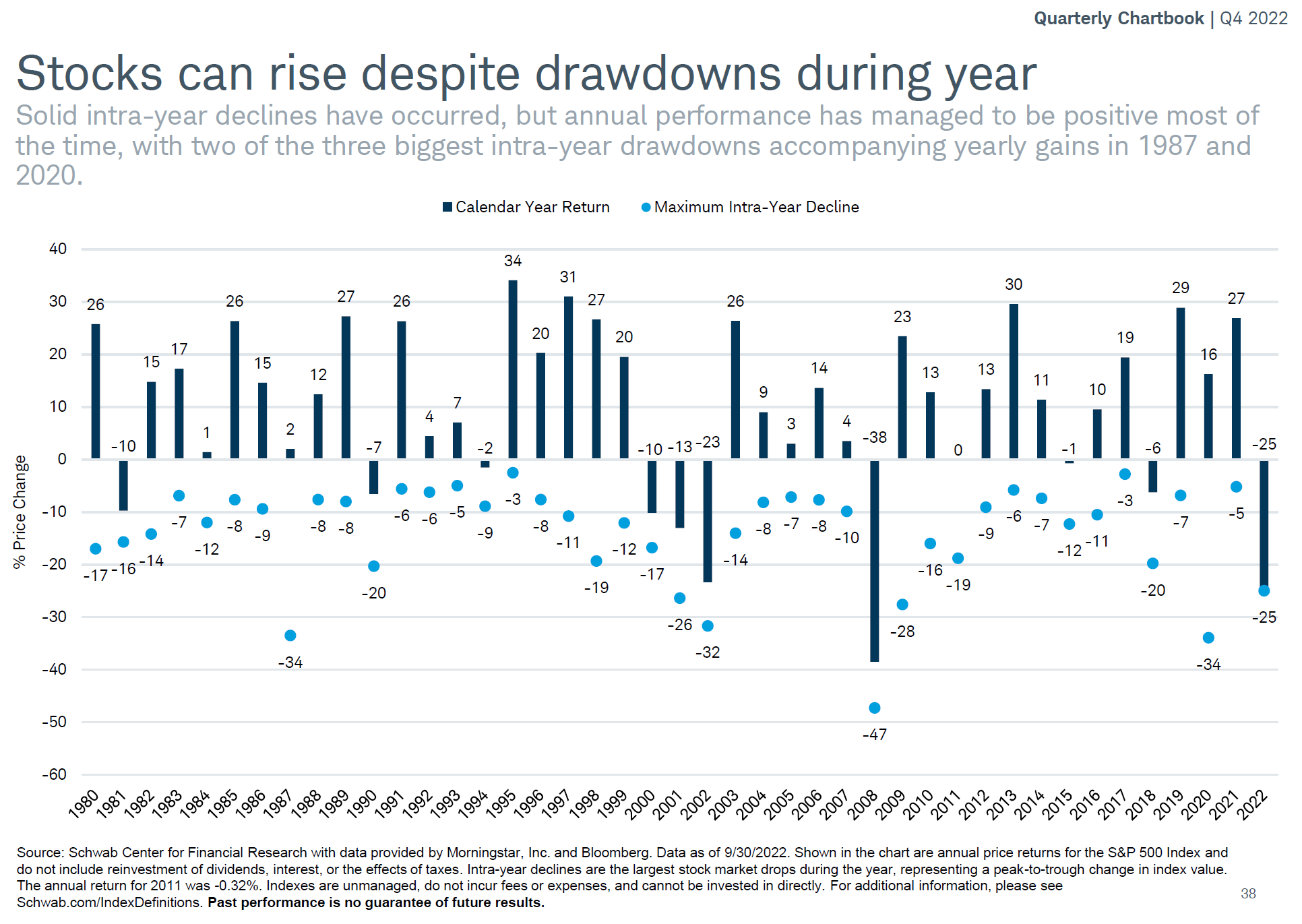

The financial headlines for stocks in 2009 were littered with exclamations that it had been a lost decade and yet the following 10 years more than made up for the losses. Today, those same media outlets are talking about a lost decade for bonds, and at DLK we will be running our quality investment processes week in and week out selecting the appropriate bonds for our clients.

The overarching theme of the report is that government programs don’t die, they morph and change over time. The recent changes to the 529 program are Exhibit A for this and are cause for general optimism about the new Invest America accounts.

Here are the three examples of the 529 Plan expanding its scope:

- You can now roll over up to $35,000 of unused 529 funds into a Roth IRA for the beneficiary, eliminating the “use it or lose it” penalty.

- The annual federal withdrawal limit for K-12 tuition has increased from $10,000 to $20,000 per student starting in 2026.

- Grandparent-owned 529 plans no longer count as student income on the FAFSA, meaning distributions won’t reduce a student’s financial aid eligibility.

Regarding the Invest America Accounts, there has been widespread analysis of their impact, including a short summary of the benefits from the Milken Institute.

KEY FINDINGS:

- Monte Carlo simulations suggest that the $1,000 accounts would grow in value, on average, to $8,000 after 20 years, $69,000 after 40 years, and $574,000 after 60 years. These results are based on long-term modeling assumptions and should be viewed as illustrative rather than predictive.

- If the policy also permitted a tax-deductible match by employers of the children’s parents, such initial matches would double an account’s value after 20, 40, and 60 years.

- Based on studies of previous efforts to provide funded savings accounts for newborns or young children, the program should increase test scores, educational attainment, and earnings of those participating. One study suggests that minority participants from low- and moderate-income families could be three times more likely to attend college and 2.5 times more likely to graduate.

- In addition to college expenses, the program could provide start-up capital for young entrepreneurs or down payments for first-time homebuyers.

- The program could also increase financial literacy of participants and their parents, which in turn would likely increase savings rates and wealth creation.

- Since all newborns would receive the grants, the program would reduce wealth inequality.

The full report can be found here.

Thoughtfully deferring taxes – when aligned with your broader plan is often in your best interest and can significantly improve long-term outcomes. It also seems like Senator Roth is making his way onto the Mt. Rushmore of helping Americans save and plan for retirement. Here is the backstory on how the Roth IRA was created